In a closed-door meeting in Brussels in March 2022, European finance ministers confronted a dilemma. Storage levels were low, LNG terminals were constrained, and heavy industry was exposed to gas shortages. As they debated a sanctions package against Russia, an insurance executive explained how tankers would reroute and premiums would spike. The resulting decision to dilute sanctions was not driven by ideology but by energy architecture: physical bottlenecks in terminals, insurance, and grids dictated policy.

I. The oil system is a security architecture, not a fuel market

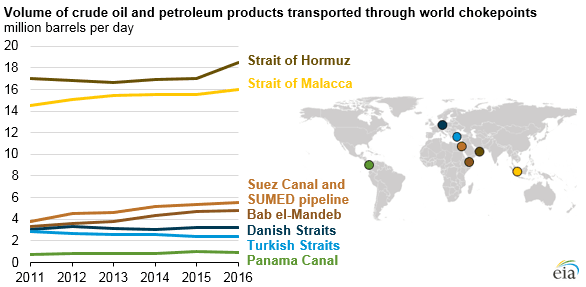

At any given moment, a significant fraction of the world's naval power is engaged, directly or indirectly, in the management of oil flows. Tankers transit narrow straits under escort. Insurance rates spike in response to distant conflicts. Strategic planners track inventories, shipping lanes, and spare production capacity with the same seriousness once reserved for troop movements. These are not the features of an ordinary commodity market. They are the features of a security system.

Oil's geopolitical importance does not arise from its usefulness alone. Coal, after all, powered industrial civilisation for a century without producing a comparable global security architecture. What distinguishes oil is the conjunction of three properties: geographic concentration, indispensability, and transport vulnerability. Large shares of global supply originate in a small number of regions, must move continuously across long distances, and are difficult to substitute in the short term. That combination converts energy into leverage.

From this leverage flow rents. States that control oil production capture revenues far in excess of extraction costs, and those revenues can be converted into durable forms of power. Domestically, they finance patronage systems, welfare bargains, or coercive security services. Externally, they translate into influence over import-dependent states, insulation from sanctions, and a degree of strategic tolerance from powers that rely on stable supply. The result is not merely wealth, but political optionality.

For the importing powers, oil dependence imposes a persistent strategic burden. Securing supply requires forward deployments, diplomatic accommodation of unsavoury partners, and the willingness to intervene in regions that would otherwise sit outside core security interests. The costs are diffuse but real: military attention diverted, fiscal resources committed, and institutional focus consumed by the maintenance of energy stability. Over decades, this burden has become normalised as part of the background condition of global order.

It is this condition, not carbon emissions, that defines oil's centrality to geopolitics. Energy security has meant controlling routes, stabilising producers, and absorbing the risks inherent in a system built around physical chokepoints. The dollar-denominated financial structures layered atop this system have reinforced it, but they are secondary to the underlying reality: oil's value is inseparable from the military and institutional machinery required to move it.

Seen in this light, the significance of fusion is not that it promises cleaner electrons. It is that, if deployed at scale, it offers an exit from a security architecture organised around scarcity, transport vulnerability, and geographic concentration. The question, then, is not whether fusion can generate power, but whether it can shift power, away from chokepoints and toward industrial capacity governed by alliances rather than geography.

II. Fusion rewires the strategic premium on oil and forces a rebuild of monetary and alliance plumbing

Fusion, when it becomes a deployable source of large-scale power, alters the strategic premium that oil has carried for decades. By reducing the importance of geographic concentration, transport vulnerability, and continuous external protection, it undermines a security architecture built around chokepoints and rents. In doing so, it compels the leading powers, particularly the United States and its allies, to rethink the fiscal, monetary, and alliance arrangements that have grown around that architecture.

This is not a prediction of geopolitical harmony, nor a claim that fusion dissolves conflict or scarcity. Energy transitions are contingent, slow, and shaped by institutions rather than technologies alone. Fusion matters geopolitically because it shifts the locus of power. Where oil concentrates leverage in specific territories and transit routes, fusion relocates leverage to industrial capacity, manufacturing scale, supply chains, regulatory regimes, and the ability to deploy and maintain complex systems over decades.

The implications of this shift extend beyond energy policy. Oil's strategic value has long justified military deployments, diplomatic accommodations, and financial structures designed to stabilise its flow. As that value erodes, the rationale for many of these commitments weakens. What replaces them will not emerge automatically. The transition away from oil-centred security will require deliberate choices about alliance coordination, industrial policy, and the institutions that anchor monetary and strategic trust.

III. New chokepoints and a governance agenda

Fusion does not eliminate chokepoints. It replaces geographic chokepoints with industrial and institutional ones. The difference is not that scarcity disappears, but that it becomes more amenable to governance. Where oil chokepoints are rooted in geography and transit vulnerability, fusion chokepoints are rooted in regulation, production capacity, and alliance coordination. This shift creates new sites of power and new opportunities for deliberate statecraft.

The first chokepoint is fuel-cycle governance, particularly tritium handling in early fusion systems. Tritium is not scarce in an absolute sense, but it is tightly regulated, difficult to handle, and politically sensitive. Control over breeding technologies, inventory management, and regulatory approval becomes a gatekeeping function. States and alliances that define standards for tritium production, transport, and accounting will shape who can deploy fusion at scale and on what terms. This is less a problem of physics than of institutional trust and compliance.

The second chokepoint is advanced materials and component manufacturing, especially superconducting magnets and associated cryogenic systems. These components sit at the technological frontier of precision manufacturing. They require specialised facilities, skilled labour, long lead times, and close integration between design and production. Supply chains in this domain are thin, geographically concentrated, and slow to replicate. Control over manufacturing capacity does not grant monopoly power indefinitely, but it does confer temporal advantage. In energy systems, time matters. Delays translate into strategic dependence.

The third chokepoint is industrial inputs and upstream supply chains, including high-purity structural alloys, specialised manufacturing equipment, and, in some designs, lithium and other materials required for breeding and structural functions. These inputs are not unique to fusion, but fusion adds sustained demand at scale. Competition for them intersects with other strategic industries, including semiconductors, aerospace, and advanced defence systems. Governance in this domain will require prioritisation, coordination, and trade-offs across sectors, rather than simple market allocation.

The fourth chokepoint is grid integration and permitting. Fusion's promise of abundant generation collides directly with some of the weakest institutional capacities in advanced economies. Transmission build-out, interconnection queues, land use approval, and regulatory harmonisation are already binding constraints for conventional generation. Fusion does not bypass them. States that cannot site, connect, and permit large-scale infrastructure will find themselves unable to translate technical capability into strategic advantage. In this sense, domestic governance becomes a central component of energy security.

What unites these chokepoints is that they are governable. Unlike oil chokepoints, they are not fixed by geography or inherited by accident. They can be shaped through standards-setting, export controls, shared infrastructure, and alliance-based industrial policy. Decisions about who participates in manufacturing consortia, who gains access to fuel-cycle technologies, and whose grids are prioritised for integration will function as instruments of power. This creates a new agenda for alliance governance. Fusion-capable states can choose to treat these chokepoints as exclusionary tools, replicating the coercive dynamics of the oil system. Or they can treat them as mechanisms for extending credible energy abundance to partners, reinforcing bloc cohesion and reducing incentives for conflict rooted in energy scarcity. The choice is not technical. It is institutional.

The strategic significance of fusion therefore lies not only in what it produces, but in how its constraints are managed. Control over these new chokepoints will determine whether fusion becomes a source of fragmentation or a foundation for a more stable and governable energy order. What replaces them will not emerge automatically. The transition away from oil-centred security will require deliberate choices about alliance coordination, industrial policy, and the institutions that anchor monetary and strategic trust.

IV. Why oil makes petrostates powerful: chokepoints, rents, and coercion

Oil confers power on states not because it is scarce in an absolute sense, but because it is scarce in strategically relevant ways. Production is geographically concentrated, substitution is slow, and transport is exposed. These features create chokepoints, both physical and institutional, through which energy must pass. Control over these chokepoints converts energy supply into political leverage.

The first source of leverage is transport vulnerability. Oil must move continuously from wellhead to refinery to consumer, often across long distances and through narrow maritime passages. Any credible threat to disruption, whether from conflict, embargo, or instability, generates immediate price effects and downstream economic risk. This gives major producers influence that can exceed their share of output, particularly in tight markets. It also gives import-dependent powers an incentive to treat distant regional stability as a core interest. The commodity becomes a security imperative.

From this vulnerability flow rents. Because demand is relatively inelastic in the short and medium term, supply constraints translate quickly into higher prices rather than reduced consumption. Producers therefore capture revenues well above marginal extraction costs. Those revenues are politically liquid. They can be mobilised without the slow institutional work required to broaden the domestic tax base, raise productivity, or win consent through inclusive growth.

Domestically, rents underwrite state capacity in two distinct ways. They finance patronage and welfare bargains that stabilise ruling coalitions, and they finance internal security services that can suppress dissent when bargains fail. Either way, the regime's survival becomes less dependent on the productive dynamism of society as a whole. Rents can decouple the state from its citizens. In the limiting case, the state becomes a mechanism for distributing hydrocarbon proceeds and maintaining order, rather than a mechanism for building a high-trust, high-productivity polity.

Externally, rents buy insulation and optionality. Sanctions and diplomatic pressure are blunted by the fear of supply shocks. Importers often hesitate to impose the full costs of coercion on producers when those costs would be paid immediately in domestic inflation, industrial disruption, and political backlash. Leaders in energy-importing democracies govern societies that experience oil disruptions as immediate, visible pain.

A separate layer of power sits above these material mechanisms. Oil trade is entangled with the monetary and financial structures of the postwar order. The Bretton Woods system tied currencies to the dollar and the dollar to gold at a fixed rate, and it eventually broke under the strain of global dollar overhang and US balance-of-payments pressures. The United States ended dollar convertibility to gold in 1971, and the early 1970s marked the transition to a floating-rate monetary world. In that environment, maintaining deep global demand for dollar assets became strategically valuable.

This is where the “petrodollar” idea is best understood as plumbing rather than ideology. After the oil shocks, major producers accumulated large dollar surpluses. Those surpluses could not be efficiently absorbed domestically at comparable scale, so they sought foreign assets. Over time, a pattern emerged in which oil revenues were recycled into US financial markets, including US Treasury securities, through a set of institutional arrangements and intermediaries. One well-documented example is the long-running US–Saudi financial channel that helped route Saudi surplus into US debt markets. The significance is not that the dollar's reserve role depends only on oil. It is that oil surpluses, recycled into dollar assets, reinforced US monetary and fiscal flexibility, and tightened the linkage between Middle Eastern stability, global energy pricing, and the dollar-centred financial system.

IV.1. Two case studies

Two case studies illustrate how these mechanisms translate into power and risk.

IV.1.a. Saudi Arabia

The relationship between the United States and Saudi Arabia has rested on an enduring strategic bargain: security assurances and defence cooperation, in exchange for reliable energy supply and a stabilising role in global oil markets. The arrangement has roots in the 1945 meeting between President Roosevelt and King Abdulaziz aboard the USS Quincy, and it has been reinterpreted by successive administrations, but its core logic has persisted. The point for this essay is not to litigate the morality of that bargain. It is to observe its structural consequences. When a region becomes systemically necessary for global energy stability, it becomes systemically difficult for the leading power to disengage from its internal politics. Commitments that began as energy security become entangled with regional rivalries, regime durability, arms sales, and the management of ideological spillovers.

IV.1.b. Russia

Russia demonstrates how hydrocarbon revenue translates into strategic endurance. In 2021, oil and gas revenues constituted roughly 45 percent of Russia's federal budget. That dependence creates vulnerability to price shocks, but it also creates capacity when prices are favourable and export volumes hold. It funds discretionary spending, foreign reserves accumulation, and the coercive apparatus of a security state. During the war period, Russia has continued to run sizeable budget deficits while sustaining high levels of defence and security spending, with the fiscal picture shaped in large part by oil and gas revenues, sanctions evasion, and war expenditures. The lesson is not that oil guarantees victory. It is that rents can extend a regime's ability to absorb pain, delay adjustment, and externalise costs onto adversaries and domestic populations.

These are the political physics of oil. Chokepoints and rents generate leverage. Leverage funds state capacity and coercion. Monetary and financial channels amplify the system's inertia. Once this is understood, the geopolitical meaning of fusion becomes clearer. Fusion threatens to erode the specific pathway through which geography becomes power. It does not end competition among states. It changes what states must control in order to compete.

V. What fusion changes: from geographic scarcity to industrial scarcity

If oil concentrates power through geography, fusion concentrates power through industry. The transition does not abolish scarcity. It relocates it. The binding constraints move inward, from deserts and straits to factories, supply chains, regulatory regimes, and institutional capacity. Energy security becomes less a problem of guarding routes and more a problem of building, maintaining, and governing complex systems at scale.

The first shift is manufacturing. Large-scale fusion deployment requires the repeated production of highly specialised components, including superconducting magnets, vacuum vessels, precision power electronics, and cryogenic systems. These are not commodities that can be sourced opportunistically on global spot markets. They require long lead times, skilled labour, quality control, and tight integration between design and production. States and firms that can industrialise fusion hardware reliably, rather than merely demonstrate it in bespoke facilities, acquire durable advantage.

The second shift is supply chains. Fusion systems depend on a narrow set of critical inputs that are difficult to substitute quickly. Superconducting materials, high-purity structural alloys, specialised manufacturing equipment, and fuel-cycle components all sit upstream of reactor operation. Control over these supply chains confers leverage, not because others cannot eventually replicate them, but because replication takes time, coordination, and institutional competence. In a world where energy demand continues to grow, delay itself becomes a source of power.

The third shift is services and maintenance. Unlike oil, which is extracted, shipped, and burned, fusion reactors are capital-intensive systems that operate over decades. They require continuous monitoring, scheduled component replacement, software updates, and fuel-cycle management. Firms and states that control the service layer, including maintenance contracts, licensing, and technical support, shape long-term dependency relationships. This mirrors the political economy of civil aviation, nuclear fission, and advanced defence systems more than it resembles hydrocarbon trade.

The fourth shift is domestic institutional capacity, particularly grid integration and permitting. Even abundant generation is strategically useless if it cannot be connected to demand. Fusion's promise therefore collides with some of the least glamorous, and most binding, constraints in advanced economies: transmission build-out, interconnection queues, land use approval, and regulatory harmonisation. States that can align permitting, financing, and grid expansion convert fusion capability into real power. Those that cannot will find abundance stranded behind institutional bottlenecks.

Taken together, these shifts alter the map of energy geopolitics. Power no longer accrues primarily to states that control territory endowed with hydrocarbons. It accrues to states and alliances that can organise industrial ecosystems, standardise designs, mobilise capital, and sustain complex systems over time. Energy security becomes less about external stabilisation and more about internal competence.

This transformation has a direct geopolitical consequence. Because industrial capacity is governable through alliances, standards, export controls, and shared infrastructure, fusion lends itself to bloc formation rather than unilateral dominance. The strategic question becomes who can extend credible energy abundance to partners, under what conditions, and through which institutions.

VI. Russia and the Gulf after oil rents: less leverage, more instability risk

If fusion weakens the strategic value of oil over time, the effects on petrostates will be uneven and delayed. Oil rents do not disappear abruptly, and states that rely on them retain substantial capacity during the transition. The long-run direction, however, is clear. As energy systems become less dependent on geographic concentration and transport vulnerability, the coercive leverage and fiscal flexibility historically conferred by oil begin to erode. The principal danger lies not in sudden irrelevance, but in instability during decline.

Russia illustrates both the present leverage of hydrocarbon rents and the counterfactual world that emerges when that leverage is absent. On the eve of the invasion of Ukraine, oil and gas revenues accounted for a large share of Russia's federal budget and an even larger share of its export earnings. That revenue base supported foreign reserve accumulation, sustained a large security apparatus, and insulated the regime from short-term economic shocks. It also shaped the strategic environment in which Western responses were formulated.

A plausible counterfactual clarifies the role of energy dependence. Had Europe and its allies entered the 2022 crisis with credible energy independence, the strategic calculus on both sides would have shifted materially. Western governments would have faced fewer constraints on sanctions design, timing, and scope. Concerns about immediate inflationary pressure, industrial disruption, and political backlash would have carried less weight. Energy price spikes would have been a secondary effect rather than a primary limiter of response. Under those conditions, the cost imposed on Russia by financial and trade sanctions would likely have been sharper, faster, and more difficult to mitigate.

The counterfactual cuts both ways. Russia's own decision-making was conditioned by the expectation that Europe's dependence on Russian gas would moderate Western escalation and fracture allied resolve. Energy leverage did not guarantee strategic success, but it reduced perceived downside risk. Oil and gas rents also extended Russia's capacity to absorb punishment once the war began, financing deficits, sustaining defence spending, and delaying fiscal adjustment. In a world where those rents were structurally weaker, Russia's margin for error would have been narrower, and the threshold for initiating large-scale military action higher.

The Gulf monarchies face a different configuration of the same underlying dynamic. Their oil rents have financed domestic stability, ambitious development programmes, and expansive welfare systems. They have also anchored a long-standing security relationship with the United States and its partners, rooted in the centrality of Middle Eastern energy to the global economy. As fusion reduces the strategic necessity of that energy, the external foundations of this bargain weaken.

In the long run, credible alternatives to oil reduce the geopolitical premium attached to Gulf stability. External powers gain greater freedom to recalibrate commitments, while regional states face stronger pressure to diversify economic and political models. Some have already begun this transition through sovereign investment, industrial policy, and controlled social reform. These efforts may succeed, but they remain constrained by institutional capacity, demographic pressures, and political risk.

As with Russia, the medium-term transition carries heightened instability risk. States accustomed to durable rent streams may respond to fiscal uncertainty with sharper regional competition, internal repression, or attempts to extract concessions before leverage dissipates. The paradox of declining strategic value is that it can increase volatility in the short term even as it promises long-term relief.

The broader implication is that fusion does not deliver an automatic peace dividend. It reshapes the incentive structure under which petrostates operate and under which energy-importing alliances respond. By reducing the ability of oil producers to convert geography into strategic restraint on others, fusion alters both the likelihood of aggression and the range of credible responses to it. Managing this shift deliberately, rather than discovering it under crisis conditions, is a central task of future statecraft.

VII. The petrodollar question: when energy is no longer the strategic commodity

Discussions of energy transition often collapse quickly into claims about the end of the dollar. This essay takes a narrower and more defensible position. The dollar's international role does not rest solely, or even primarily, on oil trade. It rests on the depth of US financial markets, the credibility of US institutions, and the security guarantees that anchor the postwar order. At the same time, energy trade has been one important structural pillar of that system. As fusion reduces the strategic centrality of oil, that pillar weakens, and the monetary architecture built around it must adjust.

The historical sequence matters. When the Bretton Woods system broke down in the early 1970s, the United States entered a world of floating exchange rates and expanding global dollar liquidity. In that environment, maintaining demand for dollar assets became strategically valuable. Large oil producers, particularly after the price shocks of the 1970s, accumulated persistent current-account surpluses denominated in dollars. Those surpluses required deep, liquid destinations. US Treasury securities and US financial markets filled that role. Over time, oil trade and oil surplus recycling reinforced the dollar's central position by linking energy stability to US fiscal and financial capacity.

This arrangement is often described imprecisely as the “petrodollar system.” In practice, it is better understood as a set of reinforcing flows rather than a formal regime. Oil producers did not hold dollars out of ideological loyalty. They held them because dollar markets were liquid, secure, and scalable, and because the United States underwrote the security environment that made oil trade possible. Energy trade did not create dollar primacy on its own, but it helped stabilise and deepen it.

Fusion alters this structure indirectly. By reducing the strategic necessity of oil, it reduces the scale and persistence of hydrocarbon-linked surplus recycling. Fewer dollars are generated automatically through energy trade, and fewer surplus flows seek safe harbour solely because oil must be priced and settled continuously. This does not produce an immediate alternative reserve currency, nor does it dissolve the dollar's advantages. It removes one source of inertia that has historically reinforced dollar demand.

What replaces it is unlikely to be a single commodity or mechanism. Reserve demand in a fusion-enabled world will be shaped less by energy settlement and more by a combination of security provision, market depth, and control over critical industrial inputs. States and firms will hold assets in currencies backed by alliances capable of guaranteeing physical security, regulatory predictability, and access to advanced industrial ecosystems. Monetary trust will increasingly track institutional competence rather than resource endowment.

This shift carries implications for US strategy. If energy trade no longer performs as much of the background work of sustaining dollar demand, the United States must rely more explicitly on what has always underpinned its monetary position: credible security guarantees, open and liquid markets, and leadership in advanced production. Fusion strengthens this position if it is deployed as part of an allied industrial system. It weakens it if it is treated as a narrow technological success detached from broader institutional design.

The petrodollar question, properly understood, is therefore not about collapse or replacement. It is about re-anchoring monetary leadership in a world where energy abundance no longer flows automatically through hydrocarbon chokepoints. Fusion accelerates that re-anchoring by shifting the basis of strategic value from extraction to production, and from geography to governance.

VIII. What is to be done? Fusion as statecraft

If fusion is treated as a narrow climate or technology programme, its geopolitical effects will be accidental and uneven. If it is treated as statecraft, it becomes a tool for reshaping alliances, reducing exposure to coercion, and rebuilding institutional capacity that has atrophied under decades of energy dependence. The difference lies not in physics, but in how deployment is organised.

Because the United States uniquely combines deep capital markets, alliance-embedded standards authority, export-credit capacity, and security provision, fusion must be organised through US institutions if the post-petrodollar energy system is to retain a stable centre of gravity. The objective is not merely to generate abundant power, but to channel the strategic rents of fusion through US institutions and supply chains, just as the petrodollar system anchored monetary primacy. What follows outlines how US agencies and their close allies can convert fusion from a scientific achievement into a durable foundation of geopolitical advantage.

First, an Allied Fusion Standards Consortium should be established under US chairmanship. This body would define interoperable design standards, quality-assurance protocols and safety benchmarks for reactors and their subsystems. By controlling the standards regime, Washington ensures that all commercially viable fusion machines are built to specifications that favour US industrial capabilities and regulatory preferences. The Department of Energy and Department of Commerce would convene the consortium, with national laboratories, reactor manufacturers and allied regulators participating on terms set in Washington.

Second, the United States should create an export-credit facility that channels foreign demand for fusion hardware and services through US supply chains. By financing the production and deployment of reactors, tritium-handling equipment and other long-lead-time components in USD and on favourable terms, the Export-Import Bank and the Treasury can entrench the dollar's role in the fusion economy. Allied export-credit agencies would be invited to co-finance under US rules, but the pricing, risk-sharing and contract law would remain American.

Third, a tritium governance framework must be stood up that preserves US leverage over the fuel cycle; rogue states in the global south are less likely to act up if we can turn the lights off. Tritium accounting, transport and recycling should operate under shared rules agreed through the US Nuclear Regulatory Commission and the International Atomic Energy Agency. Those rules must ensure non-proliferation and equitable access, but also require that any significant tritium transaction clears through US-controlled monitoring protocols. This would give Washington visibility into, and potential veto power over, global fuel flows.

Fourth, Washington should launch a components and materials industrial-base programme to secure domestic supply chains for high-field magnets, cryogenic systems, power electronics and neutron-resistant materials. The Departments of Defense (Department of War) and Energy would align defence-industrial funding with fusion requirements, while Commerce would coordinate industry consortia to expand US manufacturing capacity. Allied production would be welcome, but critical chokepoints would remain under US jurisdiction.

Fifth, permitting and transmission for fusion deployment must be fast-tracked as a matter of national security. The Federal Energy Regulatory Commission, state public-utility commissions and regional transmission operators should develop accelerated procedures for siting reactors and connecting them to the grid, with Congress granting limited federal pre-emption where local obstacles threaten strategic timelines. Abundant generation is only a source of power if it can reach demand centres under US control.

Sixth, export controls should differentiate sharply between adversarial exclusion and allied inclusion. The Departments of Commerce and State need to update the Export Administration Regulations to restrict critical fusion technologies from adversaries while facilitating intra-bloc exchange and co-production. Harmonising control lists with allied trade ministries would allow trusted partners to participate in the ecosystem without diluting US primacy.

Finally, service-and-maintenance regimes should be institutionalised as alliance-binding instruments. Reactor maintenance, refuelling and upgrades ought to be provided through long-term contracts that tie foreign operators to US vendors. National energy ministries and defence procurement authorities would negotiate framework agreements that embed support services within alliance structures, ensuring that the life-cycle of every deployed reactor reinforces US strategic centrality.

IX. Conclusion: power after scarcity

Energy systems shape the distribution of power long before they register as technologies. They determine which constraints bind, which risks can be imposed, and which actors enjoy strategic tolerance. For much of the modern era, oil has performed this organising function by tying energy supply to geography, transit vulnerability, and rents. The result has been a world in which access to fuel routinely outweighs other strategic considerations, and in which coercive behaviour by key producers is met with hesitation rather than response.

This hesitation has not been abstract. Dependence on petrostates has repeatedly limited the willingness of energy-importing powers to enforce norms against aggression, repression, and indirect violence. States whose revenues derive from hydrocarbons have been able to underwrite internal security services, external proxies, and sustained military campaigns while remaining partially insulated from sanctions and diplomatic isolation. The constraint has not been a lack of legal authority or moral clarity, but a structural fear of disruption: inflation, industrial shock, and domestic political backlash triggered by energy scarcity. In this environment, state sponsors of terrorism and revisionist actors have operated with wider margins of impunity than the international system formally allows.

Fusion alters this condition by shifting the locus of constraint. As energy supply becomes less dependent on geographically concentrated extraction and vulnerable transport, the strategic penalty for enforcement falls. The ability of producers to translate fuel control into restraint on others weakens, and with it the structural tolerance that has accompanied oil dependence. Energy security no longer requires accommodation of regimes whose behaviour would otherwise trigger isolation. It requires competence in production, regulation, and alliance coordination at home.

The implications are cumulative rather than utopian. Fusion does not eliminate conflict, nor does it dissolve the incentives for coercion. It changes which strategies are viable. When energy abundance is governed through industrial systems embedded in alliances, sanctions become sharper tools, enforcement becomes more credible, and the cost of confronting aggression shifts away from domestic populations and onto those who initiate it. Power is exercised less through scarcity and more through exclusion from production networks, standards regimes, and long-term service relationships.

This is why the governance of fusion matters as much as its deployment. Organised through fragmented markets, it risks reproducing familiar asymmetries under new technical conditions. Organised through allied standards, controlled fuel cycles, and shared industrial capacity, it supplies the institutional structure required for a more stable order: one in which energy dependence no longer compels silence, and in which coercion is met with response rather than accommodation.

The measures outlined in § VIII follow from this reality. They are not instruments of technological triumphalism, but of strategic discipline. Fusion offers an opportunity to exit an energy system that has repeatedly constrained enforcement and enabled impunity. Whether that opportunity produces a more peaceful world depends on whether abundance is treated as a problem of governance rather than as an end state. The transition away from petrostates does not guarantee restraint, but it removes one of the deepest structural obstacles to it. By lowering the domestic political and economic costs of enforcement — through reduced exposure to energy shocks — this removal makes sanctions and collective responses more credible, narrowing the gap between stated principles and feasible action.